|

Action in the precious metals and gold sector equities over the past twelve months has been highly volatile and has been disguised by the net moves of a marginally lower price (~1.5%) for US$ gold, ~12% lower for US gold indices and the gain of ~9% for the ( ASX:XGD) Gold Index. ASX:XGD) Gold Index.

The Quarterly Volatility (price range/last qtly close) in these same markets has been 9% for US$ gold, 21% for US gold stocks and 19% for the (ASX:XGD) Gold Index. This is a lot of action.

The sentiment in the sector however, especially here in the XGD, has been very poor over the past few months and some stocks have acted as if it was 2013 (-61%) MISERY TIME again. This is on top of the 41% pullback in the XGD from its July 2016 highs to those Dec 2016 lows.

This volatility makes it difficult for both investors and traders but those seeking yield and those utilising superior stock picking skills can still outperform the averages as has been the case since mid 2013.

The bigger picture for these markets has been that the annual volatility in the XGD in the past decade since 2006 has actually been even higher at 28% with -21%, -26% and a -61% figures accompanying the gains of 28%, 29%, 38% and 54%.

This volatility has made the sector stress-inducing and has pushed away many investors but the Dawes Points outlook is that the next decade should be much steadier with dividend paying stocks giving the market some defensive character and that higher gold prices should provide some large gains. The typical post-new high pullback in the 2000-2008 bull market was ~25% so hopefully an upward trending market will make these sorts of pullbacks understandable and bearable.

You have probably also noticed changes in the key Van Eck GDX and GDXJ ETFs have caused havoc as portfolios have had some structural changes on stock weightings. Some stocks were increased or added and others were reduced or cut. The triple weighted ETFs effects have been even bigger.

Changes here in the (ASX:XGD) (S&P ASX All Ordinaries Gold Index) have seen the number of stocks rise to 27 for June Qtr 2017 after being 52 in 2011 at the top (8499 in April 2011) and just 20 at the low (1642 in November 2014). I have asked this previously but is there anyone out there with a professional view on an index that has so much variation in the number of components?

Having said that it appears the XGD at last looks like an index of gold stocks with the last non-gold company removed.

With the increased population of the XGD market share of value turnover is rising above 4% and was 5% for each of the last two weeks of April.

Whatever the position here it is clear that with the A$ gold price back up around A$1,700/oz and with the generally strong (despite some abnormally heavy rainfall) March Qtr reports out there some gold stocks that are just brilliant value at current levels.

The tables below also show the high volatility but also it is pleasing to see market outperformance by some stocks in 2017. In particular, two stocks referred to in Dawes Points in 2017, CDV (+104%) and SWJ (+68%) have provided some of the best performances and Dawes Points-preferred stocks NST and TBR/RND developing the Zuleika Shear gold fields, low cost SBM, WGX, GOR and PNR have also shone through.

Site visit was made in February this year to CDV’s Namdini Project in Ghana where the 4moz deposit has had drilling indicating depth extension from 350m to 550m and potential additional mineralisation along strike. Market cap is around A$200m so with 6moz or more we could be looking at A$35-40/ inferred oz. The key feature here is the mineralising fluids passing through metamorphosed sediments, volcanics and intrusives to give 30-50m intersections. Gold recoveries are straight forward and the strip ratio is low. Gold Fields has bought 6.4% on market plus a further 7% through listed options.

A site visit to Stonewall’s (SWJ:ASX) projects at Pilgrim’s Rest in Eastern Transvaal provided further evidence of a major gold field here with 7moz already extracted from 43 mines over a strike length of 60km. SWJ has released 905koz @ 11.1g/t at Rietfontien and 1.0moz @ 6.6g/t at the Beta Mine but these are just the start. Gold production is scheduled for 2018 from upgraded existing facilities. Substantial upside possible here.

NST’s Zuleika Shear activities have been outstanding with the high grade Rubicon-Hornet-Pegasus and Raleigh mines in the EKJV producing excellent production results but more importantly, exploration drilling at all these mines will result in a significant resource upgrade.

NST will have the new 100% 50kozpa Millennium mine producing development ore by in the Sept Qtr. NST also has a very active exploration programme along the Zuleika Shear with seven rigs drilling out a resource at the very exciting Paradigm project (107m @3.1g/t and 197m @2.4g/t) .

This goldfield will just get better! Don’t forget (ASX:TNR) which is very well positioned here too.

Special mention is also made of HAV and ABU since 1 July 2016.

Dawes Points has had a couple of false starts with suggestions of gold stocks moving higher in a new upleg but with the recent pullbacks it now seems clear that time frames are longer than expected so short term rapid gains are not yet with us.

However, investors should note that many ASX Small Caps are being hammered so it is not just gold stocks!

ASX XEC S&P Emerging Companies Index 2002 -2017

This also suggests these stocks are now in coming into strong support levels and trading on good volumes.

Nevertheless the outlook is unchanged.

Gold demand from China and India continues unabated and is absorbing new mine production and Western inventories.

The Fear Trade of banking collapses, Middle East problems, North Korea and debasement of currencies are also there but are not as relevant just now.

The Bank of England recently released details of gold it holds on behalf central banks and commercial banks.

I am not really sure what it actually means but it could be reinforcing the transfer of gold from the West to the East. Almost 2,000t was removed from 2013 ……

…with another 800t exitting the SPDR Gold ETF over much the same period...

Substantial tonnages of gold have moved East and have been tightening the market in the West.

The underlying strength in the US$ gold is being reflected in the gold price in other currencies and most are a few % stronger against the US$.

Gold in US$ is just looking brilliant and a sustained break above US$1270 and more importantly above US$1300 should see a very strong move.

The internal strength of US$ gold with the 2011 high interpreted as an `irregular’ B Wave and the 2011 downtrend ready to be broken is very encouraging. The next upmove if it happens will be a Wave 3 which is typically very strong.

As noted, the trend though the various currencies is in line with this and A$ gold is already moving up. A$ gold has averaged around A$1,550 for the past six years and A$1,600 for the past two. The move back up through A$1,700 is suggesting much more to come.

Note two important currencies where gold prices look to break much higher.

Gold in Euros.

Gold in Yen.

And most importantly in Indian Rupees, the currency of the biggest buyer of gold!

India has the biggest demand for gold and gold is rising again in Rupees despite that currency rising against the US$.

Economic Outlook

Dawes Points continues to push the Global Economic Boom thesis and is encouraged by some very important recent data.

The One Belt One Road (`Belt Road’) across Asia to Europe is gaining traction with infrastructure spending picking up everywhere and is best displayed by crude steel production in China which hit a new record high rate of 847mtpa in March 2017.

India achieved 108mtpa in March after finally exceeding the magic 100mtpa in January and will very soon pass Japan to become the world’s second largest steel producer.

China can not only be expected to have robust steel production but should see at least 5% growth in 2017 as this seasonal turning point has occurred at such a high output level.

Investors seeking a play in this Asia-MENA infrastructure play should look at recent listing JC International (ASX:JCI) Calendar 2016 EPS A$0.16, Cal 2017 (E) A$0.18 and PER 4.5x.

Iron ore prices, particularly sub-60% Fe ores, have been weak but as the low grade China port stockpiles are run down at these attractive prices it can be expected that iron ore prices will be firmer into the Dec Half of 2017.

Higher grade iron ore products such as magnetite are in strong demand and the South Australia potential mega projects Iron Road (ASX:IRD), Magnetite Mines (ASX:MGT), Carpentaria (ASX:CAP) and Havilah (ASX:HAV) deserve further attention.

The US economy appears to be gaining strength through housing, manufacturing and employment but it is interesting to see on the aggregate consumption side how the US Transportation Sector has increased its share of total primary energy by 30% since 1990 from 25% to around 33% today and the underlying growth in consumption has a robustness about it.

It has been notable over the past couple of years that consumption of transportation fuels has shown double digit growth in many major economies. The underlying demand for oil is probably far stronger that the market place appreciates. Global consumption is now just over 95 MMbopd (~35bn bbls pa) and growing at 1.2-1.3MMbopd so it is going to be difficult to maintain output in the next few years. Keep in mind Australia’s largest oilfield was Kingfish in the Bass Strait with all of about 1.1bn bbls and Bass Strait itself has produced over 4bn bbls.

Whilst Peak Oil is no longer fashionable it must be recognised that most conventional reservoirs outside of the Middle East are in decline and the exploration and development outlook for near term new non-OPEC oil supply is at the lowest level since the 1940s.

The graphic below shows that in the past five years less than 6bn bbls per year has been found.

Demand is still rising but supply is struggling to keep up.

All these numbers, together with the aggregate figures given on consumption of the industrial metals suggests that the overall global production to reserves equation is increasing. Higher prices are inevitable.

So many markets are making new highs from the US, Europe, India and ASEAN and reflect strong underlying economic conditions.

It is interesting that the North Korea issue is not rating highly on the market’s radar.

Most importantly, the Sth Korean KOSPI Index is hitting new record highs!

What do they know that we don’t? Is reunification now about to happen?

There is no FEAR trade here!

Someone needs to turn on the lights!

Barry Dawes

BSc F Aus IMM (CP) MSAFAA

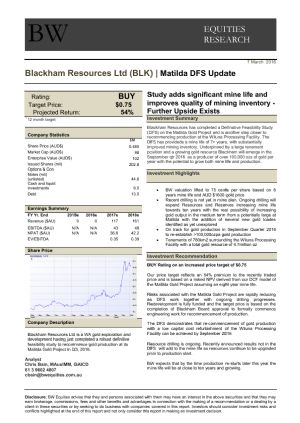

I own JCI NST, BLK, SWJ, TBR, TNR, CDV

Call me if you would like to:-

- Set up a portfolio

- Participate in Section 708 capital raisings for sophisticated investors

+61-2-9222-9111

bdawes@mpsecurities.com.au

Dawes Points #64

2 May 2017

|

Martin Place Securities is Australia's Boutique Resources Investment Firm, specialising in emerging mining, resources and energy companies.

Martin Place Securities is Australia's Boutique Resources Investment Firm, specialising in emerging mining, resources and energy companies.